.webp)

CBSE Class 12 Accountancy Practice Papers 2024: CBSE Board Exams 2024 are knocking at the doors and students might be in need of authentic study materials to refer to and practise from. Practice papers are one such important resource to build onto your knowledge about the subject and provide you with sufficient practise opportunities. Here, you can find the CBSE Class 12 Accountancy practice paper for upcoming board exams. The paper has been designed in relevance to the official sample paper released by the board since the question paper will be coming in a similar format. We have tried to provide you with all the important questions along with their answers and a PDF download link of the same.

CBSE Class 12 Accountancy Practice Paper

Find here CBSE Class 12 Accountancy Practice Paper 2024 with solutions for the upcoming CBSE 12th Accountancy Board Exam 2024. The practise paper provided below is based on the sample paper, exam pattern, and marking scheme laid down by the board. We have tried to be as precise as we could be in terms of chapter-wise weightage in the paper.

| Q.No | PART A (Accounting for Partnership Firms and Companies) | Marks |

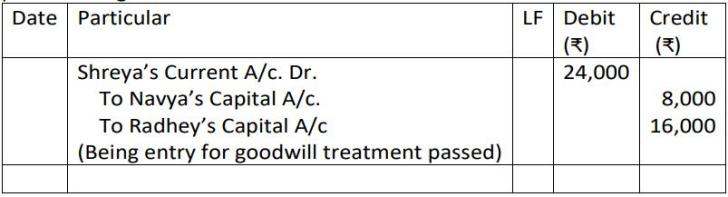

| 1 | Navya and Radhey were partners sharing profits and losses in the ratio of 3: 1. Shreya was admitted for 1/5th share in the profits. Shreya was unable to bring her share of goodwill premium in cash. The journal entry recorded for goodwill premium is given below: The new profit-sharing ratio of Navya, Radhey and Shreya will be: a) 41:7:12 b) 13:12:10 c) 3:1:1 d) 5:3:2 | 1 |

| 2 | Calculate the amount of second & final call when Abhijit Ltd, issues Equity shares of ₹10 each at a premium of 40% payable on Application ₹3, On Allotment ₹5, On First Call ₹2. a) Second & final call ₹3 b) Second & final call ₹4 c) Second & final call ₹1 d) Second & final call ₹14. | 1 |

| 3 | If 10,000 shares of ₹10 each were forfeited for non-payment of final call money of ₹3 per share and only 7,000 of these shares were re-issued @₹ 11 per share as fully paid up, then what is the minimum amount that company must collect at the time of re-issue of the remaining 3,000 shares? a) ₹ 21,000 b) ₹ 9,000 c) ₹ 16,000 d) ₹ 30,000 OR On 1st April 2022, Galaxy ltd. had a balance of ₹8,00,000 in Securities Premium account. During the year company issued 20,000 Equity shares of ₹10 each as bonus shares and used the balance amount to 1 write off Loss on issue of Debenture on account of issue of 2,00,000, 9% Debentures of ₹100 each at a discount of 10% redeemable @ 5% Premium. The amount to be charged to Statement of P&L for the year for Loss on issue of Debentures would be: a) ₹30,00,000. b) ₹22,00,000. c) ₹24,00,000. d) ₹20,00,000. | 1 |

| 4 | Samiksha, Arshiya and Divya were partners in a firm sharing profits and losses in the ratio of 5: 3: 2. With effect from 1st April 2022, they agreed to share future profits and losses in the ratio of 2: 5: 3. Their Balance Sheet showed a debit balance of ₹ 50,000 in the Profit and Loss Account and a balance of ₹ 40,000 in the Investment Fluctuation Fund. The market value of an investment is ₹30,000 against the book value of ₹50,000. Partners have decided, not to show revised valued in the balance sheet and to pass an adjusting entry for it. Which of the following is the correct treatment of the above?

OR Sohan and Mohan are partners sharing profits and losses in the ratio of 2:3 with the capitals of ₹ 5,00,000 and ₹ 6,00,000 respectively. On 1st January 2022, Sohan and Mohan granted loans of ₹ 20,000 and ₹ 10,000 respectively to 1 the firm. Determine the amount of loss to be borne by each partner for the year ended 31st March 2022 if the loss before interest for the year amounted to ₹ 2,500. a) Share of Loss Sohan –₹ 1,250 Mohan – ₹ 1,250 b) Share of Loss Sohan –₹ 1,000 Mohan – ₹ 1,500 c) Share of Loss Sohan –₹ 820 Mohan – ₹ 1,230 d) Share of Loss Sohan –₹ 1,180 Mohan – ₹ 1,770 | 1 |

| 5 | What will be the correct sequence of events? (i) Forfeiture of shares. (ii) Default on Calls. (iii) Re-issue of shares. (iv) Amount transferred to capital reserve. Options: (a) (i), (iv), (ii), (iii) (b) (ii), (iv), (i), (iii) (c) (ii), (i), (iii), (iv) (d) (iii), (iv), (i) (ii) | 1 |

| 6 | Alexa Ltd. purchased building from Siri Ltd for ₹8,00,000. The consideration was paid by issue of 6%debentures of ₹100 each at a discount of 20%. The 6% Debentures account is credited with: a) ₹10,40,000 b) ₹10,00,000 c) ₹9,60,000 d) ₹6,40,000 OR Which of the following statements is incorrect about debentures? a) Interest on debentures is an appropriation of profits. b) Debenture holders are the creditors of a company. c) Debentures can be issued to vendors at discount. d) Interest is not paid on Debentures issued as Collateral Security. | 1 |

| 7 | Attire Ltd, issued a prospectus inviting applications for 12,000 shares of ₹10 each payable ₹3 on application, ₹ 5 on allotment and balance on call. Public had applied for certain number of shares and application money was received. Which of the following application money, if received restricts the company to proceed with the allotment of shares, as per SEBI guidelines? a) ₹ 36,000 b) ₹ 45,000 c) ₹ 30,000 d) ₹ 32,400 | 1 |

| 8 | At the time of reconstitution of a partnership firm, recording of an unrecorded liability will lead to: (a) Gain to the existing partners (b) Loss to the existing partners (c) Neither gain nor loss to the existing partners (d) None of the above | 1 |

| 9 | The amount to bereflected in blank (1) will be: a) ₹37,200 b) ₹44,700 c) ₹22,800 d) ₹20,940 | 1 |

| 10 | Choose the correct sequence of the following transactions in context of Division of Profits. (a) Guarantee by Firm to Partners (b) Guarantee by Partners to Firm (c) Transfer of Profits to Profit and Loss Appropriation Account (d) Guarantee by Partner to Partner a) (i); (iii) ; (iv) ; (ii) b) (iii); (i) ; (ii) ; (iv) c) (iii) ; (ii) ; (i); (iv) d) (ii); (iii); (iv); (i) | 1 |

For complete CBSE Class 12 Accountancy Practice Paper 2024, click on the link that follows

Importance of Practice Papers for Board Exams

Practice papers can prove to be a great source of uplifting performance in the exam. Check below why practice papers are so important for board exams.

- Informs students about the question paper format and marking scheme, since they are based on sample papers

- Consists of important questions. Hence, provides students with an idea of the types of questions asked in the exam

- Adds to the understanding of the subject and examination

- Helps students in analysing their weak and strong points

- Adds to the list of study materials to be used by students in strengthening their performance

Important Resources for Preparation of CBSE Class 12 Accountancy Board Exam 2024

| CBSE Class 12 Accountancy Important Assertion Reasoning Questions |

Comments

All Comments (0)

Join the conversation